Those who have chosen to invest in gold bars or to buy silver coins have often done so because they fear the mismanagement of the monetary system. This week has offered further reassurance that investors are right to want to own gold in a balanced portfolio because yet another fight about the US debt ceiling has concluded. The conclusion is always the same: ‘keep kicking that can’. Whilst Congress ‘celebrates’ reaching a new deal on the country’s national debt, regular citizens and the rest of the world brace for impact.

Pretend and Extend

Rising interest rates are pushing over-indebted countries to their limits. Politicians and international agencies such as the World Bank and International Monetary Fund (IMF) stand on soapboxes shouting the need for fiscal constraint.

But mostly this is mere posturing or promises made to get one or more of; the debt restructuring, additional loans, or outcomes needed in the immediate situation. Fiscal constraint and ‘paying down’ debt largely seems to be a notion of the past – today’s solutions usually come down to debt restructuring monikered ‘pretend and extend’.

The deal this week to raise the debt ceiling in the U.S. is an example of this mentality. The deal ‘waives’ the debt ceiling until January 2025.

This is a precarious date, as the newly elected Congress and U.S. president take office in January 2025. Congress is sworn in at the beginning of January and the U.S. president on January 25, 2025.

The debt ceiling deal doesn’t authorize new spending but allows the U.S. Treasury to issue debt for spending already authorized by Congress. In the U.S. the Democrats want to reduce the deficit (and debt) by increasing revenues through higher taxes on corporations and upper income individuals, while Republicans want cuts on spending to be what reduces debt.

Download Your Free Guide

The growing divide between Democrats and Republicans has meant that very few from the opposite political party will support the other’s agenda. The debt ceiling deal does have some clawbacks, such as $30 billion in unspent Covid relief that wasn’t used and can’t be used now, but most of the vague provisions for spending cuts are for future years, which by then could easily be reversed or a ‘work around’ found.

The U.S. avoided default and can continue to issue debt that the market will buy. And if markets do not buy it the U.S. Treasury can turn to the Federal Reserve to snap up the excess.

Even though the U.S. is paying a much higher interest rate this year compared to the last several years, it can continue to pay the interest on that debt by issuing more debt. For other countries, this is not the case, however. The rise in interest rates has pushed other countries to the brink and now a sovereign debt crisis is lurking.

Lurking Sovereign Debt Crisis

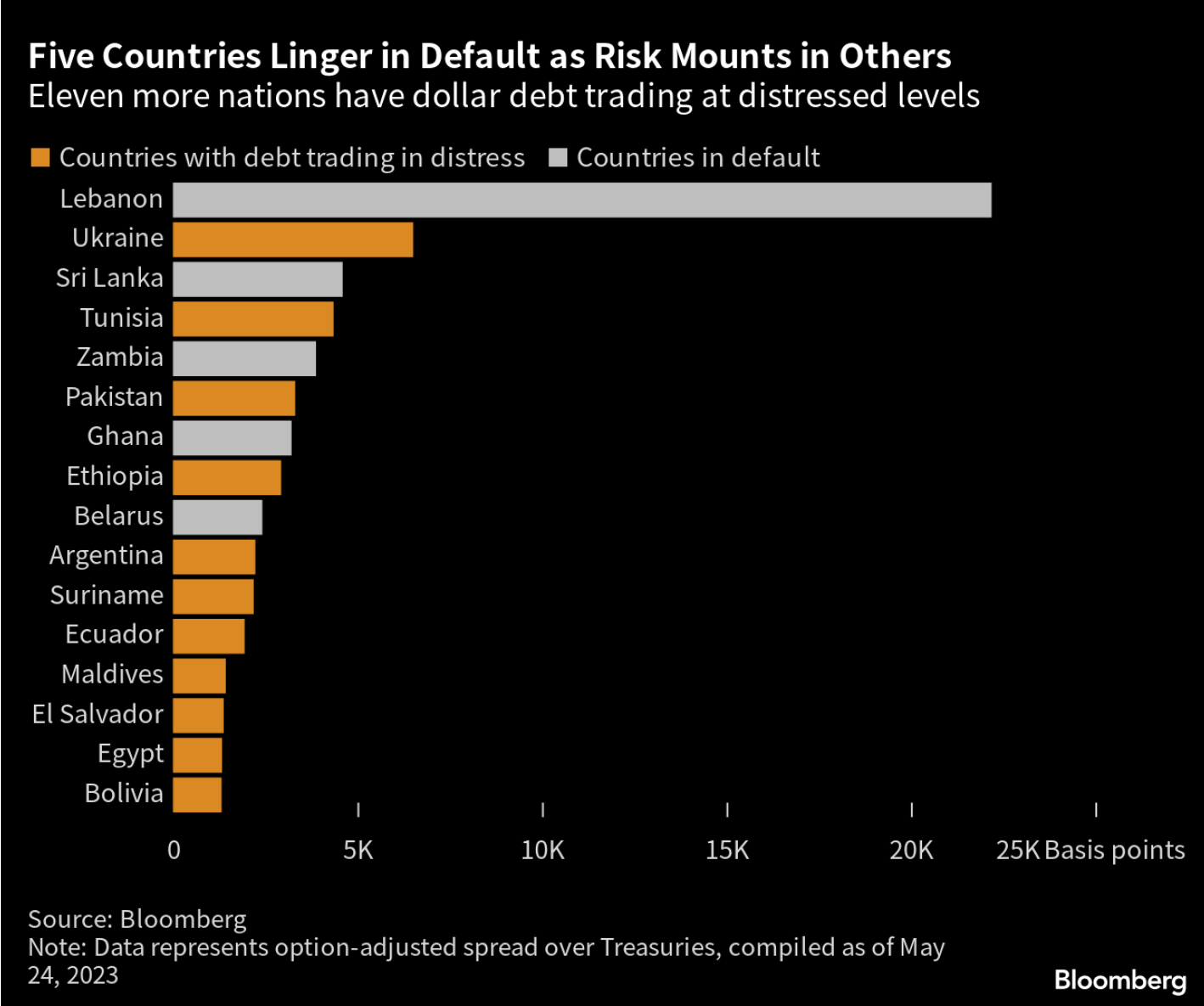

Bloomberg reports this week that government defaults rise to a record in the developing world, and the debate is growing frantic over how to solve these debt crises. Restructuring talks are stalling, with some countries turning to old-school sweeteners and others calling to revamp the Group of 20’s Common Framework.

The additional government debt issued during covid coupled with the rapid rise in the U.S. dollar post covid has pushed five developing countries into default with eleven others identified as trading at distressed levels.

The Group of 20 Common Framework was “launched in 2020 as a mechanism to provide a swift and comprehensive overhaul to nations buckling under debt burdens after Covid-19 shock that would reach beyond temporary debt payment moratoriums.”

However, to date, no country has been able to utilize the new framework. This means that many poorer countries have been locked out of markets for financing ongoing government budgets. During the time of the lockout, it is indeed very difficult for the country, and recession is generally imminent.

Typically, once an agreement is reached the debt is restructured. Creditors usually suffer some losses and in time the market ‘forgets’. After everyone has forgotten the subject country sees borrowing costs come down again and the government borrows until the cycle repeats.

Moral Hazard is Rising

The elephant in the room is that moral hazard is rising – governments and investors are counting on international institutions and central banks to step in and limit or eliminate the losses on not only government debt.

During the Great Financial Crisis and following European Debt Crisis central banks were reactive to developing crises in financial markets and sovereign debt. Post covid central banks are much more proactive in creating programs and providing guarantees.

For example, only after the crisis had erupted in Greece and contagion was feared across the Eurozone did the ECB create the Outright Monetary Transactions programme to buy distressed debt. Furthermore, this program was only accessible after the government with the distressed debt negotiated with the European Stability Mechanism a bailout or a line of credit.

In contrast, last year, when the ECB started raising rates, the ECB created the Transmission Protection Instrument (TPI) as a precaution in case markets perceived that a country’s debt was in crisis.

This immediately lowered the spread between countries’ debt in the Eurozone (for example Italy’s 10-year yield declined by around 75 basis points, to a spread of 185 basis points above Germany’s 10-year yield). In order to access the TPI countries only need to be “in broad compliance” with the bloc’s fiscal rules, but even this is subjective as Italy’s debt to GDP is 144.4%, with a deficit of 8% of GDP in 2022.

The previous general bloc’s fiscal rule of debt to GDP of under 60% and a deficit of under 3% of GDP is being re-evaluated and will be more subjective to each country’s fiscal situation.

Gareth Soloway – This is the catapult that will send gold to new highs

The ECB has not been ‘challenged’ by the market to carry out its promise of support yet, but in our view, as interest rates rise further that day is coming in the not too distant future, as it is for other countries outside the currency bloc.

How long the era of ‘pretend and extend’ on sovereign debt will continue has yet to be seen – but eventually eras and cycles shift and usually the pendulum swings far in the other direction before moving back. Gold and silver investors will be rewarded when it does shift.

From The Trading Desk

Market Update:

The gold price has bounced off its recent lows close to $1,930 and is trading back above $1,960 this morning.

We have seen over the last couple of weeks clients coming in buying the recent dip, cost averaging, and adding to their allocations.

Macro news this week, a deal has been agreed on the US debt-celling, which removes the big piece of uncertainty on the US economy.

Tomorrow US Non-farm payrolls will be released.

A strong job number will fuel expectations of another hike looking more likely when the Fed next meet on June 14th.

However, any signs of the labour market cooling and a lower CPI print released the day before (June 13th) the Fed’s next scheduled meeting could change all that with some forecasters saying inflation has peaked.

Stock Update

Silver Britannia’s– We have a limited number of Silver Britannia’s from the Royal Mint, with the lowest premium in the market at spot plus 40% for EU storage/delivery and for UK storage/delivery.

Gold 1oz Bars and Coins – GoldCore have excellent stock and availability on all Gold Coins and bars. Please contact our trading desk with any questions you may have.

Buy Gold Coins

GOLD PRICES ( AM/ PM LBMA FIX– USD, GBP & EUR )

| USD $ AM | USD $ PM | GBP £ AM | GBP £ PM | EUR € AM | EUR € PM | |

|---|---|---|---|---|---|---|

| 31-05-2023 | 1959.00 | 1964.40 | 1585.03 | 1588.41 | 1835.78 | 1841.23 |

| 30-05-2023 | 1949.50 | 1952.45 | 1570.32 | 1571.14 | 1818.88 | 1820.27 |

| 26-05-2023 | 1953.50 | 1947.90 | 1580.97 | 1577.02 | 1819.69 | 1816.22 |

| 25-05-2023 | 1962.30 | 1948.25 | 1585.15 | 1579.64 | 1828.08 | 1817.72 |

| 24-05-2023 | 1976.80 | 1969.65 | 1592.91 | 1590.69 | 1833.68 | 1828.43 |

| 23-05-2023 | 1959.65 | 1969.20 | 1581.05 | 1585.99 | 1815.81 | 1826.24 |

| 22-05-2023 | 1981.20 | 1970.30 | 1591.70 | 1585.30 | 1831.22 | 1822.92 |

| 19-05-2023 | 1965.55 | 1961.60 | 1582.86 | 1577.52 | 1821.48 | 1817.42 |

Buy gold coins and bars and store them in the safest vaults in Switzerland, London or Singapore with GoldCore.

Learn why Switzerland remains a safe-haven jurisdiction for owning precious metals. Access Our Most Popular Guide, the Essential Guide to Storing Gold in Switzerland here

Receive Our Award Winning Market Updates In Your Inbox – Sign Up Here